Presentation by Yoon Jong Lee, Vice President of DBHiTek

[Semicon Korea 2019]

"Foundry investment in China is becoming a threat, and the pace of the threat to Korea will be accelerated."

Chinese and overseas major foundry companies are rapidly expanding production facilities in China. As demand for semiconductors in China rises, foundries are increasing their 12-inch wafer production facilities and focusing on high-tech nodes.

Yoon Jong Lee, Vice President of DBHiTek, said, "The growth of the semiconductor industry in China is fierce," at the press conference held at Semicon Korea 2019 held in COEX, Seoul on the 23rd. "There are four leading Chinese foundry companies," he explained. Those four are SMIC, HHGrace, HLMC, and CSMC. By last year, SMIC and HHGrace each had a monthly production capacity of 430,000 units and 170,000 units, respectively. In 2020, They are expected to increase to 580,000 and 190,000 units monthly, respectively. In the same year, HLMC and CSMC will each have a production capacity of 140,000 units and 120,000 units per month. "Factory utilization rates are another issue, but they are not so small," he said.

VP Lee noted that, in addition to the issue that Chinese companies have large-scale facilities, overseas major foundries have recently expanded their investment in China. TSMC (Taiwan) and Global Foundry (US) also secured new production facilities in China last year. He believes that China and foreign foundry companies' investment in China will be a major threat to Korea. The speed at which it becomes a threat will be even faster.

China and overseas major foundry companies are focusing on expanding their 12-inch wafer fabrication facilities. Last year, TSMC, Global Foundry, and SMIC all increased their 12-inch facilities. In 2020, HLMC and HHGrace will also increase their 12-inch facilities. At the same time, foundry companies are expected to maintain their 90% utilization rate at 8-inch production facilities. Last December, TSMC announced plans to expand its 8-inch fab.

There are also foundry companies growing bigger with mergers and acquisitions (M&A). Israel TowerJazz and Taiwan Vanguard are the leading examples. TowerJazz recently increased its position in the foundry business ranking by acquiring the facilities of Panasonic and Maxim. A new factory is also under construction. In the entire foundry market, the share of TSMC, Global Foundry, UMC, and SMIC is still overwhelming at 82.9%. Korea's DBHiTek ranks 10th with 1.1%.

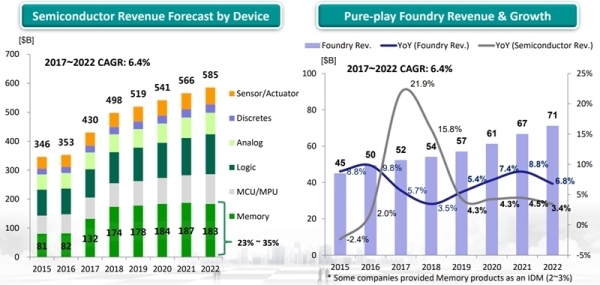

The 2019-2022 foundry market is expected to grow by 7.1%. This is higher than the overall semiconductor market growth at 4.1%. USB type C, the 3D image sensor (ToF), optical FPS, and automobiles are leading the growth. All estimates of CAGR from 2018-2020 are more than double digits. In particular, optical FPS grows at a CAGR of 151%. The Fourth Industrial Revolutions such as the Internet of Things (IoT), AI (Artificial Intelligence), and 5G also help foundry companies to increase their sales. Since 2017, the foundry operation rate has been at 90%.

Since the 2000s, as fabless companies have grown steadily, foundry companies have had many opportunities. Major fabless Qualcomm sales rose from $ 15.4 billion in 2016 to $ 17.1 billion in 2017, while Broadcom sales rose to $ 16.1 billion in 2017 from $ 13.8 billion in 2016. In contrast, the integrated device manufacturer (IDM) has seen a sharp drop in its investment in fab since 2013.

In the foundry process technology, 7nm is expected to become a new mainstream technology. TSMC and Samsung Electronics foundry have entered the production of 7-nanometer since last year. In the 32~28nm business, the issue of overcapacity is continuing due to the intensified competition among the top four companies and other foundry companies. The 0.18 micrometer is still in demand as a major legacy technology.

The overall semiconductor industry sales have been steadily rising recently. In 2016~2018, the average sales price of memory semiconductors (ASP) rose, and the market also grew significantly. In 2018, the memory revenue accounted for 35% of the total semiconductor industry. The memory sales have doubled to the level compared to that in 2016.